Ireland Herd Number BPS Payment Tracker

0

Free download

CT1 corporation tax workings template with profit, add-backs, capital allowances, losses, tax liability and balance for Irish companies.

Download template

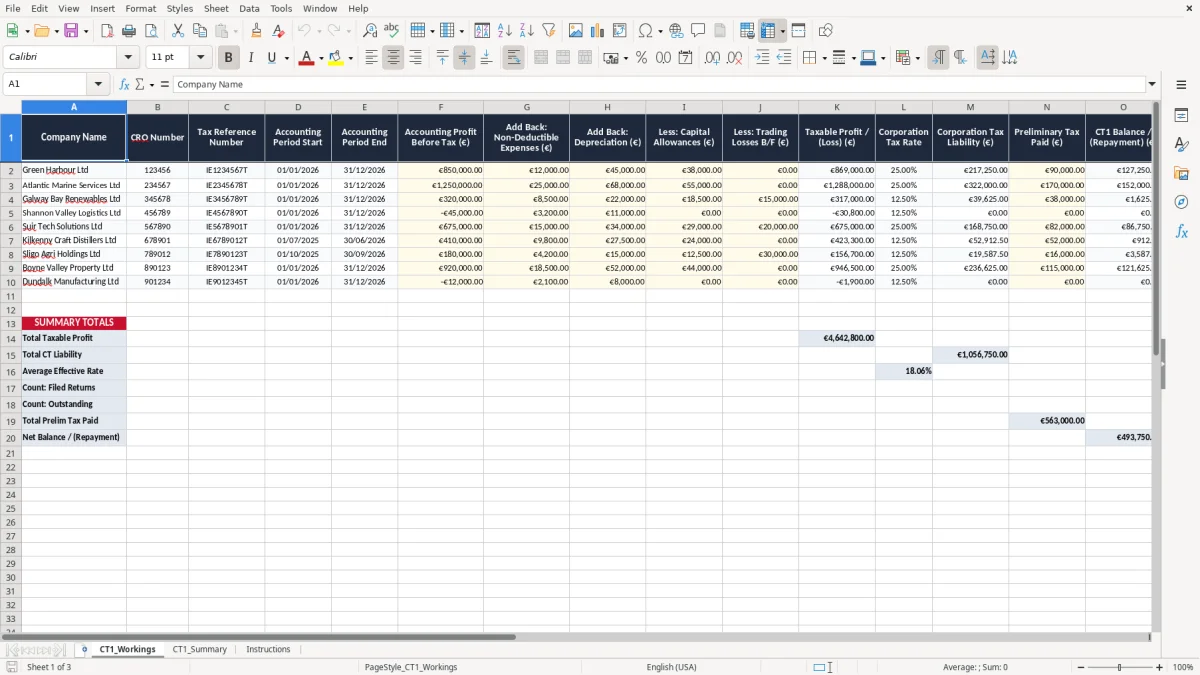

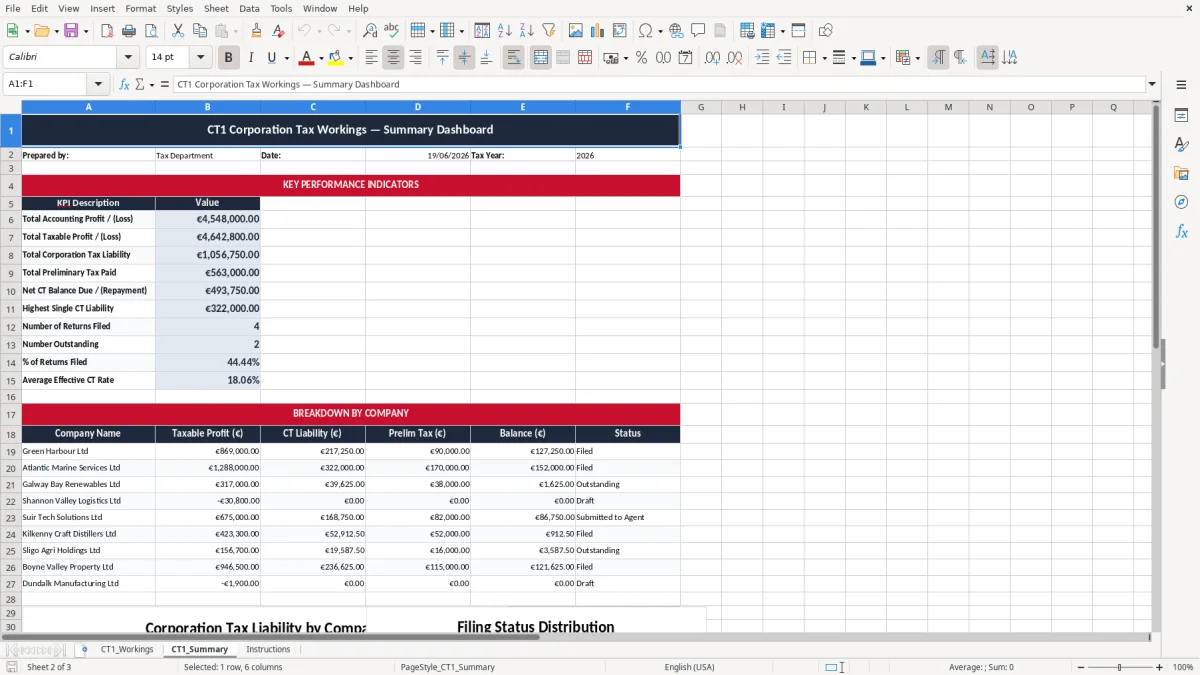

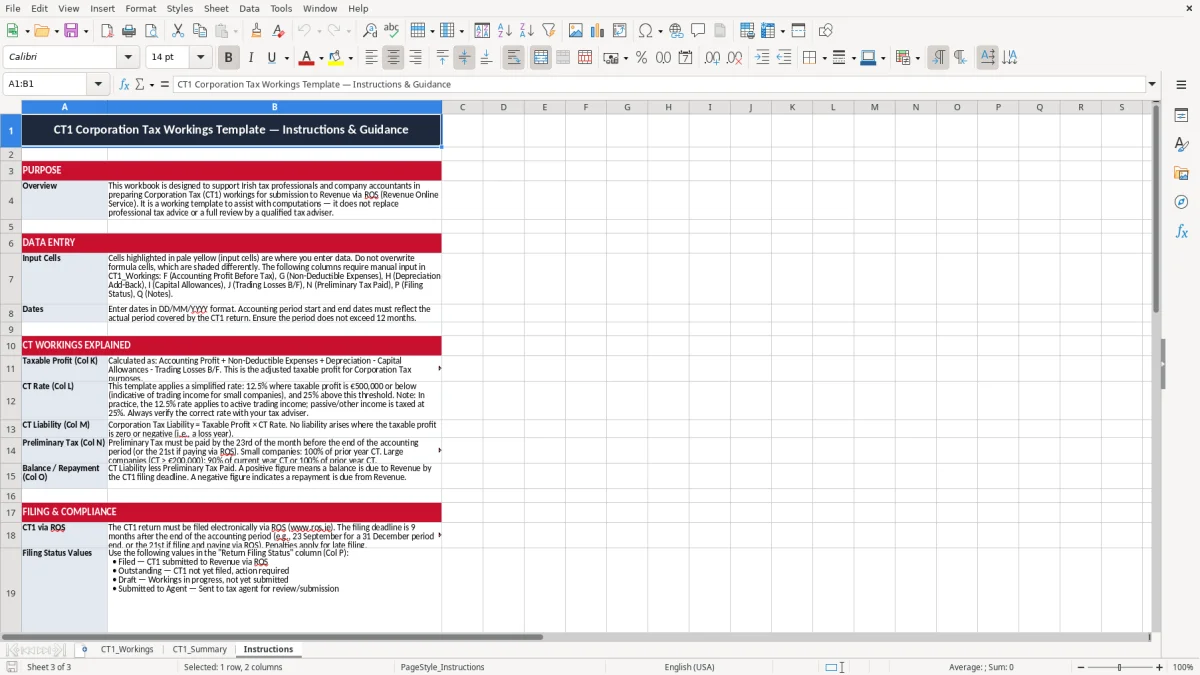

This CT1 corporation tax workings Excel template helps you calculate a company’s taxable profit, corporation tax at 12.5%, preliminary tax paid and any balance due or repayment. It includes CT1_Workings, CT1_Summary and Instructions sheets so you can track the figures you need before filing with Revenue.

Use it for a limited company’s year-end tax computation, especially when you need to pull together accounting profit, non-deductible expenses, depreciation, capital allowances and trading losses brought forward. The workbook is set up for Irish companies filing a Form CT1 through ROS.

The layout suits a bookkeeper, director or accountant who wants one place for the working papers and a cleaner summary for review. The screenshots show the inputs on the workings sheet, the summary view and a short instructions tab for filing.

A CT1 workings sheet is for the people who have to turn draft accounts into a tax computation before the Form CT1 goes to Revenue. In practice that is usually a bookkeeper in a small limited company, an external accountant doing year end, or a director who wants to understand the tax bill before money leaves the bank.

The workbook is useful when the accounting period has ended and you need to separate accounting profit from taxable profit. A company with €180,000 profit before tax, €12,000 of entertainment disallowed and €38,000 of capital allowances needs a clear trail, not a blank notebook.

The pressure point is usually year end and the months leading into the Form CT1 filing. If the company has already paid preliminary tax, you need the balance quickly so the director can decide whether to hold cash back or clear the liability.

Take a plumbing company with 4 employees and €420,000 turnover. If accounting profit is €96,000, add-backs are €8,500 and capital allowances are €21,000, the taxable profit drops to €83,500 before the 12.5% rate is applied. That is exactly the kind of working a spreadsheet is better at than a calculator and a pile of notes.

For an Irish trading company, corporation tax on trading income is 12.5%. If the company has €80,000 taxable trading profit, the corporation tax liability is €10,000 before preliminary tax is set against it.

Revenue expects the numbers to be supported by records kept for 6 years, and the company should be able to show where each add-back or deduction came from. Depreciation is not a tax deduction, so you add it back in the computation and then claim capital allowances separately where the asset qualifies.

The sheet helps you keep the accounting treatment and tax treatment apart. For example, €6,000 of depreciation on a van is added back, while qualifying wear and tear capital allowances may be claimed at 12.5% a year over 8 years on the tax side.

The completed figures feed the Form CT1 filed through ROS. A limited company registered with the CRO uses the company tax reference details on the working paper, and the resulting balance or repayment tells you whether the preliminary tax paid was enough for the period.

The common failure is mixing up accounting profit and taxable profit. If you forget to add back €14,000 of disallowed expenses, you understate the tax bill by €1,750 at 12.5%, and that error follows you straight into the return.

Another problem is treating depreciation as if it were a tax deduction. A company can have a healthy profit and still report the wrong taxable figure if the bookkeeper leaves depreciation in the computation and forgets to claim the qualifying capital allowances instead.

Trading losses brought forward are often entered without checking the opening figure from the previous period. If you claim €50,000 of losses when only €32,000 is available, the tax computation is wrong and the company may end up with an unexpected balance due later.

Preliminary tax is another place where firms trip up. A company that paid €8,000 on account against a €10,500 liability still owes €2,500, and if nobody spots that before filing, cash flow takes the hit at the worst possible time.

Messy CT1 workings usually cost time first and money second. I have seen a one-hour review turn into a half-day rebuild because the figures were spread across emails, a spreadsheet and a PDF draft with no notes column and no clear link back to the accounts.

The same problem shows up in indirect tax, where a VAT3 workings sheet keeps the figures, notes and source links together before the return is filed.

The best way to keep this spreadsheet alive is to link it to the year-end close, not to treat it as a separate job. If you always open it when the draft accounts land, the tax computation is ready while the numbers are still fresh.

A simple 30-minute check at the end of the accounts process is usually enough for a small company with one trading activity. Once you are dealing with multiple trades, group relief, or a full tax provision across several entities, the spreadsheet starts to feel too loose and you should move the workflow into accounting software or a dedicated tax system.